The Fourth of July arrives once again, that familiar day of national celebration when Americans gather to commemorate their independence, a concept enshrined not only in political terms but woven into the very mythology of the nation itself. Across the country, there will be fireworks and parades, backyard barbecues and patriotic speeches, all evoking the enduring ideals of freedom, self-determination and the rights of the individual. Yet, for all the celebration and sentimentality, it seems rather few will pause to consider the more subtle question of what independence actually means in the modern era, particularly when viewed through the unglamorous, yet crucial, lens of personal finance and monetary stability.

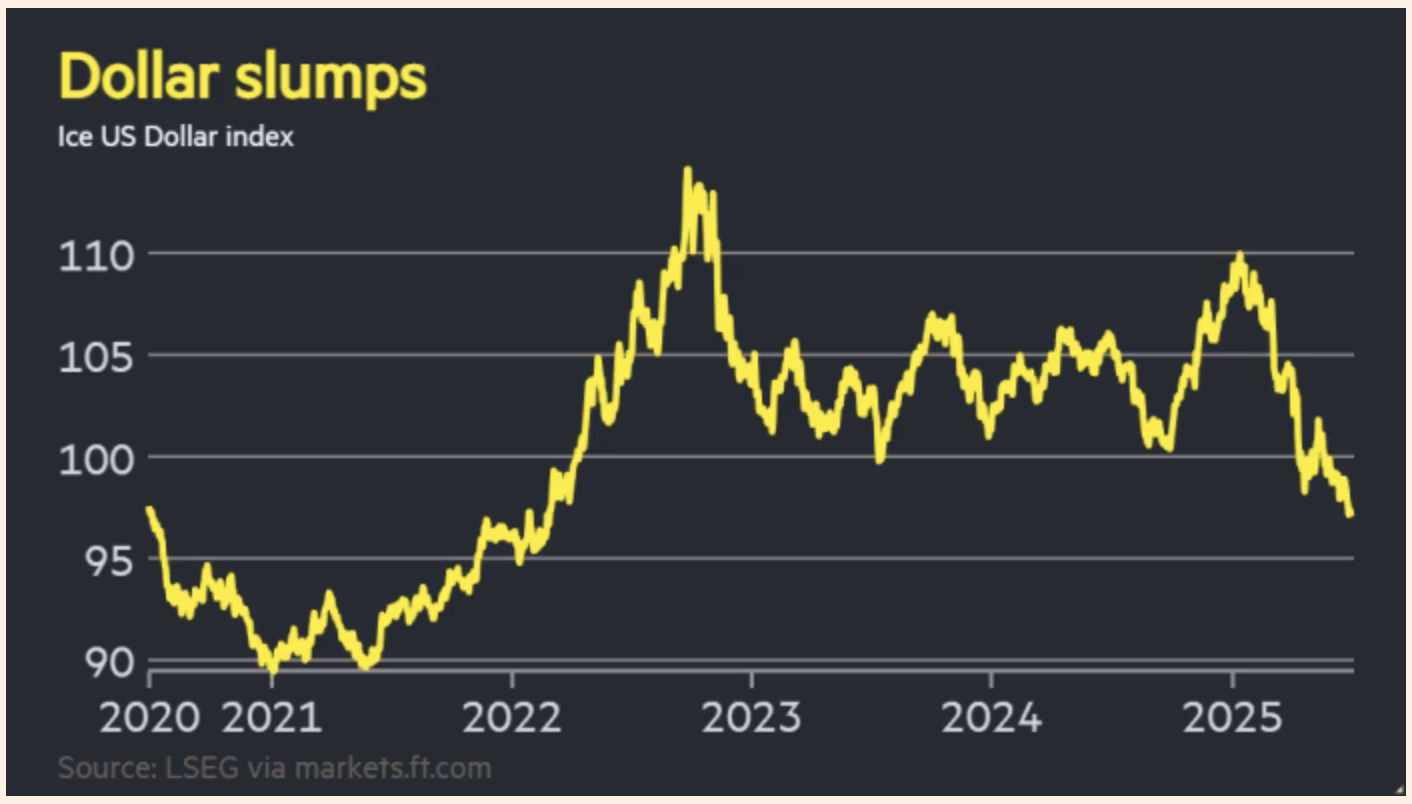

It is not fashionable to speak of such things on days like today, but it is worth noting that the US dollar, long assumed to be as unassailable as the country itself, is suffering its worst start to a year since 1973, the very year when the last lingering connections to gold were formally severed and the dollar became entirely unmoored from anything other than the shifting tides of faith and policy. In the first six months of this year, the dollar has fallen more than ten per cent against its peers, a decline all the more striking because it comes not in response to some foreign shock or geopolitical rupture, but rather from the steady accumulation of homegrown pressures such as erratic trade policies, unrelenting deficits and mounting doubts about the Federal Reserve’s independence.

Investors, who for decades treated the dollar as a safe haven without question, are now openly reconsidering their allegiances. Increasingly, they are shifting away from US assets, hedging their exposures and placing growing confidence in alternatives such as the euro, the Swiss franc and gold, that age-old refuge from monetary folly. The underlying message in the markets is becoming harder to ignore: the dollar, for all its historical weight, is no longer immune to the forces of reappraisal. The world, it seems, is beginning to ask whether the greenback still merits the blind trust that it has enjoyed for so long.

Source: FT

This reassessment is hardly speculative. As Ray Dalio, the prominent investor and historian of financial cycles, noted this week, the fiscal trajectory of the United States is rapidly approaching a point of serious strain. The latest budget legislation, now passed through Congress, maps out a future in which government spending will remain near seven trillion dollars per year, with revenues closer to five trillion, leaving an annual gap that will be bridged only by yet more borrowing. The US national debt, already exceeding the size of the entire economy and amounting to some 230,000 dollars per household, is projected to swell to 130 per cent of GDP within a decade, which would equate to roughly 425,000 dollars per family. This, in turn, will drive interest payments to staggering levels, with total debt service costs, interest and principal combined, projected to rise from around ten trillion dollars today to eighteen trillion dollars within ten years.

Dalio, drawing on centuries of financial history, is not optimistic about how this will be resolved. He reminds us that, time and again, governments faced with such towering debts have followed a well-trodden path. They lower interest rates and devalue the currency in which their debts are denominated. This strategy has long been favoured by policymakers precisely because of its subtlety; unlike spending cuts or tax hikes, currency devaluation reduces wealth in ways that are difficult for the average citizen to fully detect. As the value of money declines, it creates the illusion that everything else is simply becoming more expensive, when in reality it is the purchasing power of the currency itself that is evaporating.

The Next Financial Crisis Has Already Begun (Few See It Coming)

What makes this all the more troubling is how calmly Americans have accepted this state of affairs. It has become commonplace, even fashionable, to discuss the need to protect savings from inflation, as if it were some natural phenomenon akin to the changing of the seasons, something to be managed and hedged against rather than challenged at its root. Financial commentators and mainstream advisers speak casually about allocating portfolios to inflation-resistant assets, as though it were entirely reasonable that a person’s accumulated savings might simply diminish in value through no fault of their own. The idea that money should preserve purchasing power over time, once a foundational principle of sound finance, now strikes many as quaint, if not outright naïve.

It is difficult to overstate the implications of this quiet shift in thinking. Americans are not merely watching their currency weaken against foreign rivals; they are experiencing a loss of purchasing power at home, in the most tangible and immediate sense, as their dollars buy less at the grocery store, the petrol station and everywhere else. This process is not theoretical; it affects households across the country every day, though it is seldom described in those stark terms.

The comparison to the United Kingdom is instructive, for while Britain faces its own struggles with political instability and fiscal credibility, at least there the discussions about monetary risk and market discipline remain somewhat more candid. Sterling has stumbled and wobbled, its fluctuations tied closely to the political dramas of Westminster, but few in Britain are under the illusion that their currency is invulnerable. The difference in America is the persistent belief, still clung to by many, that the dollar will somehow defy history and remain forever immune to the forces that have undone every other currency throughout time.

The truth, however, is that no currency is exempt from the laws of arithmetic or the limits of investor patience. The dollar’s position as the global reserve currency, long described as an exorbitant privilege, has indeed allowed the United States to run larger deficits and maintain looser fiscal standards than any other nation on earth, but that privilege, like all privileges, is contingent upon trust. And trust, once questioned, tends to erode more quickly than expected.

What, then, does true independence look like in such an environment? It surely cannot be measured by mere political sovereignty or the ability to vote every few years. Real independence, in this context, means having control over one’s financial future, being able to save and invest in a way that is insulated from the slow, relentless confiscation of purchasing power through currency devaluation and monetary mismanagement.

It is here that the case for gold, that most unfashionable of assets, reasserts itself with quiet force. Unlike paper currencies, gold cannot be printed or debased. It is not tied to the fortunes of any one government or central bank. It simply exists, steady and indifferent to political whims, as it has for millennia, serving as a store of value not because it promises returns, but because it preserves what has already been earned.

As Americans gather beneath the fireworks this evening, many will reflect on the familiar themes of liberty and independence, but fewer will stop to consider the ways in which their personal independence is being chipped away by forces that operate beyond the reach of ballots and speeches. The uncomfortable reality is that independence is not merely a national ideal; it is also a personal choice. And in an age when even the value of money itself is no longer stable, the quiet act of moving beyond the fiat system may prove to be one of the few genuinely independent choices left.

There will be no celebrations for such decisions, no flags waving or anthems sung. But in the long run, they may well prove to be the most consequential acts of all.

Buy Gold Coins

Buy gold coins and bars and store them in the safest vaults in Switzerland, London or Singapore with GoldCore.

Learn why Switzerland remains a safe-haven jurisdiction for owning precious metals. Access Our Most Popular Guide, the Essential Guide to Storing Gold in Switzerland here.

Receive Our Award Winning Market Updates In Your Inbox – Sign Up Here